Parish Council Finances

ACCOUNTS

The Parish Council aims to give excellent value for money as it raises and spends money for the benefit of the local community.

Public Money: The Parish Council makes it clear where the money goes and is accountable for sound financial management. Council tax payers have no choice but to pay up so they have a right to scrutinise the way in which the council uses their money. They also expect the council to minimise the risk to public money. Risk Management must inform the councils financial decisions. The council that spends public money has a duty to do so lawfully and using legal procedures. If a council spends money unlawfully it could be in trouble with the auditor and even the courts! The council must be confident that when it spends public money:it has legal power (it is not acting beyond its powers)it follows lawful procedures it does not take unnecessary risks transactions are transparent councillors conform to standards in public decision making. Whilst the government pushes for a professional approach to financial management they have also reduced the audit process by which the Audit commission checks the financial procedures of Parish Councils – on condition that councils demonstrate their ability to audit themselves i.e. the appointment of their own internal auditor.

BUDGETS: The budget shows how council policies are financed; it therefore represents the councils powers to: provide services work for the benefit of the community respond to local needs encourage and support groups in the local community. The budget is an agreed plan of income and expenditure for a specific financial year which runs from 1st April to 31st March. The precept is calculated as an element of the budget. The precept is the council tax which the district council collects on behalf of the parish council. It is the balance by estimating planned expenditure and subtracting planned income. The council normally reviews policies and agrees the budget and the precept in the autumn. The Responsible financial Officer (the CPC clerk) completes the precept request in December or January as required by the district council. The request is in effect a demand. The DC must provide the sum required. The budget/precept must be agreed by the full council.

What happens if you overspend during the year? There should be a contingency fund built into the budget. It is perfectly legal to move budgeted funds from one heading to another. The council can agree a supplementary budget during the year. This might involve transferring funds from reserves. The council cannot issue a supplementary precept to raise more money from the current precept. It is good practice to publicise council policies and spending plans in a way that makes the public sit up and take notice. There are numerous statutes under which the council can spend money. Parish Councils have limited powers to do whatever they choose for the local community using Section 137 of the Local Government Act 1972. If they can’t find a specific power/statute to authorise expenditure, the council can use the power of Section 137 which permits expenditure on anything of benefit to the parish or community – a local authority may incur expenditure which, in their opinion is in the interest of, and will bring direct benefit to, their area or any part of it or all or some of its inhabitants. This means that the council cannot uses S.137 if a specific power exists – some councils do not use it at all. It is illegal for a council to spend money if it has no statutory power to act. (if in doubt further advice is sought from HALC or the internal auditor) - further details of rules and regulations are within the councils Financial Regulations – which all members have a copy of Individual councillors must never commit the council to expenditure nor can they spend money on the councils behalf. The council must not agree to spend money on the spur of the moment.

AUDIT

Good governance, accountability and transparency are essential to local councils and a cornerstone of the government’s approach to improving public services. Those who are responsible for the conduct of public business and for spending public money are accountable for ensuring that public business is conducted in accordance with the law and applicable proper practices. They must also ensure that public money is safeguarded, properly accounted for and used economically, efficiently and effectively. In discharging this accountability, public bodies and those responsible for their management are required to make proper arrangements for the governance of their affairs and the stewardship of the resources in their care. They are required to report on these arrangements in their published Annual Governance Statement. As a safeguard to the proper discharge of this accountability, external auditors in the public sector give an independent opinion on public bodies’ financial statements. They may also review, and report on, aspects of public bodies' arrangements to ensure the proper conduct of their financial affairs, and those to manage their performance and use of resources.

CIL MONEY

This is money collected by a local authority from developments to support local infrastructure.

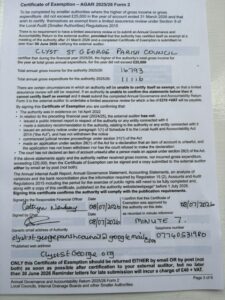

ANNUAL GOVERNANCE & ACCOUNTABILITY RETURN

Form 2 Certificate of Exemption 2025-2026 - Agar - Sent July 2026

LIST OF ASSETS